Thursday, March 31, 2022

Kohr Explores: PIR Auto Swap Meet is back - KOIN.com

[unable to retrieve full-text content]

Kohr Explores: PIR Auto Swap Meet is back KOIN.com"auto" - Google News

March 31, 2022 at 07:51PM

https://ift.tt/GSdbfXR

Kohr Explores: PIR Auto Swap Meet is back - KOIN.com

"auto" - Google News

https://ift.tt/w1jbnDS

Shoes Man Tutorial

Pos News Update

Meme Update

Korean Entertainment News

Japan News Update

Two years that changed the auto industry - just-auto.com

Covid-19 seemingly came out of nowhere in early 2020 and proceeded to impact our lives – across the world – in so many ways. The pandemic brought lockdowns and ushered in new ways of working and brought societal change. How did it impact the global automotive industry?

Living with lower volumes and supply chain fragility

This has probably been the biggest impact. Companies have been forced to manage their activities in unprecedented ways as Covid-19 shut sales markets and shuttered factories. Many are still on the learning curve in terms of understanding how to manage unexpected disruption, but at least more aware of where the business risks lay.

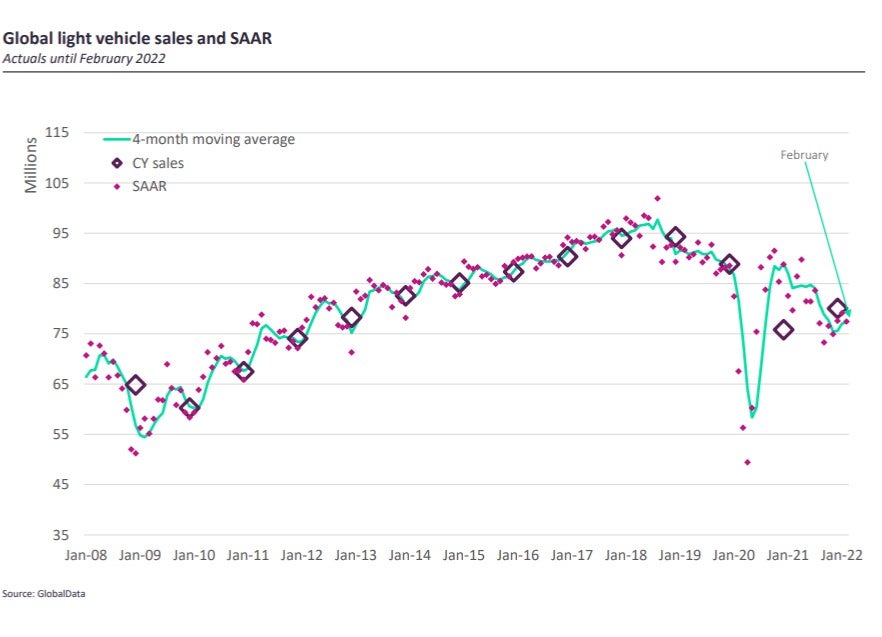

As the chart below illustrates, the global light vehicle market fell off a cliff in 2020. While there was market recovery, that recovery was uneven and blunted by supply chain problems (notably shortages of semiconductors) that constrained sales in 2021. The market remains well below pre-pandemic levels.

Population lockdowns in 2020 shuttered factories and dealerships across major markets. As Covid-19 infection rates surged, companies were faced with mandates to cease manufacturing operations and send workers home. Besides the immediate challenge of managing cash flow to pay workers when sales revenues were suddenly halted, there was a need also to understand how supply chains and factories worked. Besides suspending manufacturing activities for an unspecified period, there was the knowledge that at some point everything needed to be restarted again.

Undoubtedly there are lessons in cash management and strategic prioritization that will become pillars of many companies’ operational strategies for years to come. Early in the crisis, many companies reached for the oxygen provided by the opening of new credit lines. This buffer helped get companies over the hump of the first wave of the pandemic while later recovery in market levels, allied with a laser-like focus on costs and the bottom line, saw many players roar back to profitability in the second half of 2020.

Later in the year it was to be a generally chaotic picture with restarts as manufacturers struggled with the effects of ongoing disruption down the supply chain. The public health crisis itself was characterised by variances in responses – and indeed strategies – by national governments which meant that the volume of infections and associated economic disruptions varied considerably across the world. With long and complex supply chains spanning the globe, vehicle makers and major suppliers were caught out by both the fragility and a lack of transparency in their supply chains.

Commendably, many OEMs and major suppliers were able to repurpose their factories to make ventilators, PPE and other health equipment that was in high demand in health services.

Striving to better understand supply chains – alongside managing plants as flexibly as possible – has been given added urgency by the shortcomings shown up by the dramatic swings caused by Covid-19. Are the lessons being learnt and new solutions applied? That is harder to assess, but companies are making better use of process tools such as blockchain to manage their supply chains. Shortages of certain types of component and their costs will also have raised awareness of risk mitigation strategies inside procurement departments.

A big lesson is that the supply chain – in all its complexities – cannot be taken for granted. OEMs and suppliers need to undertake in-depth analysis of their supply chains, understand where bottlenecks are likely to occur and stratify their commodity purchases accordingly. This is what Toyota – the masters of lean production – did, in learning lessons from the Fukushima nuclear disaster, and others need to follow suit now. The cost of warehousing supplies of crucial components is minimal compared with the impact on production of supply chain breakages.

The CASE is altered

The CASE acronym that sums up four major auto industry megatrends – Connectivity, Autonomous, Sharing, Electric – has been around a while now. The letters sometimes get mixed up in other forms (ACES, for example). The relative speed and importance of the CASE constituents has been changed by the pandemic, though the shifts are subtle and overlay shifts that were happening anyway. The ‘E’ is more important now than it was pre-pandemic. The last two years have seen an acceleration in the momentum towards electrification – in terms of both market trends and supply-side activities. Investment in new electric vehicles, the required technologies (such as new vehicle platforms) and component systems (powertrain/drivetrains, especially batteries) has taken off. The pandemic also gave way to talk among politicians of ‘green recoveries’ and building back better, with rethinks, or at least a change of emphasis, evident in the political discourse surrounding topics such as transport policy and sustainability.

In many ways, electrification has been given the jump-start it needed via the pandemic. Several factors are at play here. Market incentives to assist demand have been very prevalent in Europe, where the share of BEVs sold in the market leapt from 3.16% in Q4 2019 to 9.9% in the whole of 2021. When government support for the industry came after the worst of the 2020 decline, it was frequently packaged in green wrapping paper. Government sponsored incentives have coincided with a raft of new BEVs on the market as OEMs move to meet 2021’s EU CO2 emissions target and more stringent future regulations.

The long-term residual impacts of the pandemic have still to be determined, particularly with more working from home and less demand for public transport (usage is significantly under pre-pandemic levels in the UK) as numbers of weekday commuting journeys have declined.

Lockdown and the post-lockdown environment will likely lead to individuals and households reassessing their transport needs and solutions. Modal mix could change, but it’s not necessarily going to be to the detriment of private transport. If there is less appetite for shared mobility or public transport, those fortunate enough to have the means may well have added a BEV as a purchase option or possibility for future consideration, to their household.

Sharing (through ride-hail) has undoubtedly seen some disruption due to the pandemic. The big question is whether this is a long-term shift in people’s sensibilities or whether we get a return to pre-pandemic trends. There was some recovery to rider numbers and revenues in 2021, but the Omicron variant put a dampener on things in early 2022. We have also seen the ride-hail companies pivoting their business models towards goods and food delivery.

More online retail of goods and delivery to homes has been a major contributory factory in LCV demand remaining relatively buoyant as major delivery fleets have seen their business surge. Already growing online shopping was lifted further by lockdowns that curtailed physical shopping.

UK new light commercial vehicle (LCV) registrations ended 2021 up 21.4% at 355,346 units, some 62,723 units more than in 2020 and just 2.8% down on pre-pandemic 2019 (365,778 units) – despite industry-wide semiconductor shortages which hit the market in the second half. Big fleet operators (such as Amazon) are also giving more consideration to electrified van fleets. Strongest growth last year was in the mainstay 3.5 tonne panel van segment, with 2021 sales up an astonishing 27.8% at 243,889 units. One supporting factor: vans are generally a little less advanced tech (and therefore electronics parts) intensive than passenger cars and overall volumes are lower, so they are a little more able to withstand the semiconductors shortage.

The jury is out on the ‘A’ in CASE: Autonomous. Autonomous Vehicle (AV) tech has been a big consumer of investment and R&D spend over the past five years. Besides the direct spend in R&D departments or JVs, there has also been plenty of M&A activity involving startups and tech specialists – both software and hardware. With question marks over sharing, the business case for autonomous loses some of its lustre. Much of the push for autonomous has been to see shared mobility businesses move to driverless, thus reducing fixed and variable costs and bringing the companies sustainable profitability to justify sky high stock valuations.

While ADAS systems will inevitably continue their progression, it seems doubtful presently that Level 4 and Level 5 autonomy will be seen at scale anytime soon outside of tightly policed geofenced areas.

Digitization of automotive retailing – at last

One area that has demonstrated more resilience than most is automotive retail. Since the internet’s inception, vehicle retail has looked ripe for digitization. However, for whatever reason it’s never really taken off. Sure, consumers use the net to research and evaluate their next purchases, but the customer journey never really evolved through the whole buying process. With many dealers forced to close their doors due to lockdowns, dealers and national sales companies were forced into a rapid re-evaluation to save their businesses. Never has necessity is the mother of all invention seemed more apposite.

Now, for automotive retail, it’s no longer a case of “clicks-to-bricks” but more a case of click and collect. Retailers are offering doorstep delivery of test drives and new vehicle purchases. Electronic signatures and credit checks are commonplace. In short, much of the friction has been taken out of the buying process. It’s easy to conceive that future showrooms will be just that. Places where people need to kick the tyres and can visit as part of their buying process. Everything else will be handled digitally, removing much pain from the buying process.

SUMMARY

How has the pandemic impacted the auto industry? In short, established practices and assumptions on how the industry operates have been severely challenged. In effect, there is a divide between the pre-pandemic and post-pandemic automotive worlds. While both of those worlds face the same underlying long-term megatrends, the business landscape has been irrevocably changed in many respects. Perhaps the biggest single change is in mindset and the new need to address, through strategies and agile event-reactive tactics, a world of much greater volatility and uncertainty.

Supply-side impacts and responses

- Population lockdowns across the world at different times highlighted the need for greater understanding of automotive manufacturing supply chains. Companies are grappling to develop risk mitigation strategies and embrace ‘what if’ scenario planning.

- Vehicle makers are generally working more closely with their Tier 1 suppliers on volume/order changes and identifying break points further down their supply chains.

- Manufacturers have had to adopt more flexible working processes – for example by examining plant-model mix, optimal shift patterns – so that they can adjust to larger-than-normal order volume swings.

- Investment strategies re-appraised, particularly in the areas of advanced technologies competing for capital.

- E-mobility given added momentum, for both OEMs and suppliers.

- Inventory planning. More volatility in final markets has created a need to manage flows of vehicles and aftermarket parts more carefully for final distribution channels.

Demand-side/retail impacts and responses

- Market forecasts have had to be revised quickly as demand conditions and regulations changed, often at very short notice. Agility and speed of response is key, with the right tools and analytical frameworks in place.

- Lessons in cash management and making credit lines available quickly as needed.

- OEMs have had to work with distribution groups and dealers on new protocols and processes for customer interface – both on-site and on-line. The pandemic forced some to a greater level of cooperation and collaboration than was previously the case.

- Online marketing and retail given a boost.

- Private mobility – and car ownership – potentially more attractive as modal choices for journeys as working patterns (less daily commuting) change.

"auto" - Google News

March 31, 2022 at 11:36PM

https://ift.tt/Fx6WK8M

Two years that changed the auto industry - just-auto.com

"auto" - Google News

https://ift.tt/w1jbnDS

Shoes Man Tutorial

Pos News Update

Meme Update

Korean Entertainment News

Japan News Update

EU weighs driver data rules, pitting insurers against auto giants - Reuters

/cloudfront-us-east-2.images.arcpublishing.com/reuters/A2TDWGYGTBK47MAEDHJDWBPHVM.jpg)

A policeman directs traffic at a busy street of downtown Shanghai December 5, 2012. REUTERS/Carlos Barria/

Register now for FREE unlimited access to Reuters.com

LONDON, March 31 (Reuters) - The European Union has launched a public consultation on possible rules to ensure fair access to drivers' data, pitting the powerful insurance and auto industries against one another in a battle to monetise digital information.

The bloc's executive European Commission said in a call for evidence document on Thursday that over 85% of new cars in 2018 were connected wirelessly, with more than 470 million connected vehicles expected to be on the roads in Europe, the United States and China by 2025.

The EU has already proposed a Data Act, but it may not be sufficiently detailed for handling auto data, and a further measure could standardise data sets, and ensure fair access and competition, the EU executive said.

Register now for FREE unlimited access to Reuters.com

Industry body Insurance Europe said such a measure would be the first of its kind.

Automakers have long guarded their 'gatekeeper' role in accessing data from cars, such as how fast they are being driven, with an increasing amount of information now received via wireless transmission.

Insurers and car repair shops have been lobbying the EU to allow drivers, and not the automakers, to decide who can directly access data from their vehicles.

If the automakers control the data, they can also control which insurer or other service provider covers the vehicle. read more

Putting the driver in charge would mean all industries are on the same competitive footing, Insurance Europe said.

"There is a need to regulate this, as you cannot leave this in the hands of car manufacturers," said Nicolas Jeanmart, Insurance Europe's head of personal and general insurance.

"It should be for each driver to decide what they want to do with their data, and if they want to share with an external provider like an insurer."

There are around 250 million cars on the roads in EU.

Insurers are already providing services to drivers through apps in countries such as Britain and Italy, but provision is patchy. It would be easier and cheaper to offer them directly on the basis of car data, Insurance Europe said.

European automakers industry body ACEA said Europe's auto industry was committed to giving access to the data generated by the vehicles but uncontrolled access posed cyber, data protection and privacy threats.

"That is why any EU legislative framework should keep vehicles and their occupants safe and secure," ACEA said, adding it must also guarantee the auto sector can remain competitive.

Register now for FREE unlimited access to Reuters.com

Additional reporting by Nick Carey Editing by Mark Potter

Our Standards: The Thomson Reuters Trust Principles.

"auto" - Google News

March 31, 2022 at 04:00PM

https://ift.tt/4KdUCRW

EU weighs driver data rules, pitting insurers against auto giants - Reuters

"auto" - Google News

https://ift.tt/w1jbnDS

Shoes Man Tutorial

Pos News Update

Meme Update

Korean Entertainment News

Japan News Update

Tuesday, March 29, 2022

Passport Auto Group gives 300 residents free gas | WDVM25 & DCW50 | Washington, DC - WDVM 25

[unable to retrieve full-text content]

Passport Auto Group gives 300 residents free gas | WDVM25 & DCW50 | Washington, DC WDVM 25"auto" - Google News

March 30, 2022 at 09:53AM

https://ift.tt/8uhiepT

Passport Auto Group gives 300 residents free gas | WDVM25 & DCW50 | Washington, DC - WDVM 25

"auto" - Google News

https://ift.tt/9U2v7DR

Shoes Man Tutorial

Pos News Update

Meme Update

Korean Entertainment News

Japan News Update

Despite record auto credit availability, economic 'spring chills' projected - Auto Remarketing

Tuesday, Mar. 29, 2022, 10:12 AM

Credit availability for auto financing in February rose to the highest level that experts have seen in seven years. But fueled in part by soaring prices, including for new vehicles, conditions prompted one expert to project that the U.S. economy is “in for some spring chills.”

That’s the gist of recent analysts from Cox Automotive, Moody’s Analytics and S&P Global.

"auto" - Google News

March 29, 2022 at 09:12PM

https://ift.tt/GaUZ8oB

Despite record auto credit availability, economic 'spring chills' projected - Auto Remarketing

"auto" - Google News

https://ift.tt/9U2v7DR

Shoes Man Tutorial

Pos News Update

Meme Update

Korean Entertainment News

Japan News Update

Monday, March 28, 2022

U.S. auto sales slump as less affluent buyers walk away - Reuters.com

/cloudfront-us-east-2.images.arcpublishing.com/reuters/SYFQALYHSZNWFHZ6FBM54NBESQ.jpg)

Cars unsold due to the autos market slowdown caused by coronavirus disease (COVID-19) are seen stored in the parking lot of the Wells Fargo Center in Philadelphia, Pennsylvania, U.S. April 28, 2020. REUTERS/Mark Makela

Register now for FREE unlimited access to Reuters.com

March 28 (Reuters) - U.S. new vehicle sales could fall to the lowest first-quarter volume in the past decade as chip shortages and the Ukraine crisis squeeze inventories and rising prices push less affluent buyers out of the market, research firm Cox Automotive said Monday.

U.S. car and light truck sales are expected to fall more than 24% to about 1.22 million units in March and decline more than 16% in the first quarter.

"Make no mistake, this market is stuck in low gear," said Charlie Chesbrough, senior economist at Cox Automotive, adding that sales will remain at current levels until supply improves.

Register now for FREE unlimited access to Reuters.com

Cox forecasters said the U.S. economy should not experience a recession. But Cox cut its forecast for U.S. car and light truck sales in all of 2022 to 15.3 million vehicles, down 700,000 vehicles from its January outlook. And even hitting the new target will require significant improvement in supply chain disruptions, Cox said.

Fresh lockdowns in China as well as Russia's invasion of Ukraine have reignited supply bottlenecks that were easing over recent months. Tight supplies have pushed new vehicle prices to record high levels. read more

Detroit's mainstream brands and NissanMotor Corp (7201.T) are getting hurt as less affluent consumers leave the new vehicle market, Cox analysts said during a call.

Households with less than $75,000 in annual income now account for nearly two percentage points less of the U.S. light vehicle market than a year ago, Chesbrough said. The average income of a new vehicle buyer is now $124,000.

Detroit mainstream brands such as Chevrolet are losing market share, while Cox predicted Japan's Toyota(7203.T) could be the top selling automaker in the U.S. market for the first quarter.

"Long-term, you are shrinking the pool of people who are likely to buy" a new vehicle, said Cox Chief Economist Jonathan Smoke.

Register now for FREE unlimited access to Reuters.com

Reporting by Kannaki Deka in Bengaluru and Joseph White in Detroit; Editing by Devika Syamnath and Tomasz Janowski

Our Standards: The Thomson Reuters Trust Principles.

"auto" - Google News

March 29, 2022 at 01:58AM

https://ift.tt/LN1oC0h

U.S. auto sales slump as less affluent buyers walk away - Reuters.com

"auto" - Google News

https://ift.tt/ZfJwWQz

Shoes Man Tutorial

Pos News Update

Meme Update

Korean Entertainment News

Japan News Update

70-year-old woman dead after auto-pedestrian crash in SLC, police say - KJZZ

[unable to retrieve full-text content]

70-year-old woman dead after auto-pedestrian crash in SLC, police say KJZZ"auto" - Google News

March 28, 2022 at 10:34PM

https://ift.tt/q7L1P30

70-year-old woman dead after auto-pedestrian crash in SLC, police say - KJZZ

"auto" - Google News

https://ift.tt/ZfJwWQz

Shoes Man Tutorial

Pos News Update

Meme Update

Korean Entertainment News

Japan News Update

How Important Could Upstart's Auto Business Be by 2032? - The Motley Fool

Upstart ( UPST -1.90% ) has taken the lending industry by storm with a platform that helps make affordable credit available to more Americans. The company's product competes primarily with the FICO credit score, which, while historically critical to lenders, is a flawed method for determining a person's creditworthiness. As a study conducted by Upstart in 2019 found, 80% of Americans have never defaulted on a debt, yet only 50% of Americans have access to prime credit based on their FICO scores.

The flaws in those simple credit score formulas have left a broad swath of the U.S. population without access to credit at affordable interest rates.

Upstart is trying to change that. Its artificial intelligence platform considers more than 1,500 variables to make lending decisions on each individual borrower. This generates a more holistic view of creditworthiness. Primarily, its determination system has been used by its lender clients to make decisions about personal loans, but in April 2021, Upstart bought Prodigy -- an auto retail software company -- to accelerate its expansion into the auto loan niche. That looks to be a major opportunity for the fintech.

Image source: Getty Images.

Customers are signing up left and right

Like the traditional personal loan business, the auto financing system has a lot of flaws. More than $1 trillion worth of cars are purchased at dealerships in the U.S. every year, and most of them get financed -- but only 1% of buyers say they are satisfied with the process. Since the Prodigy acquisition closed, Upstart has been working to do better and has grown the number of dealership locations using its platform by 106% to 410.

The number of banks that partner with Upstart to offer auto loans has also been expanding: It now has 10 bank partners on its auto platform. If the rate at which its personal loan business has grown is any guide, the number of banks using Upstart to make auto loan decisions could grow at a rapid rate: At the end of the third quarter, the company had 31 bank partners. By the end of Q4, that number had increased by 35% to 42.

Upstart has created a retail solution -- where car buyers can navigate through the entire car-buying experience -- to further the growth of its auto loan segment. This retail site connects every part of its business: It has partnered with manufacturers like Subaru and Volkswagen ( VWAGY 1.12% ) to offer cars, which can then be purchased through its dealership partners, while its bank clients finance the purchases.

It is important to note that Upstart doesn't take on any of the risk in the loans. It simply gets paid for each application determination it conducts, a business model that provides a stable and consistent revenue stream.

Optimism about the future

In the company's fourth-quarter conference call, CEO David Girouard noted that the "auto [refinancing] funnel performance is now comparable to where our personal loan funnel was in 2019." For reference, the number of loans facilitated with Upstart's AI engine grew by 527% from Q4 2019 to Q4 2021, so there could be plenty of growth ahead.

By the end of 2022, management expects that its auto loan transaction volume will reach $1.5 billion, which is incredible considering that it originated its first auto loan in late 2020. The company also generated over $135 million in net income and $153 million in free cash flow in 2021 -- funds that could be reinvested in fueling this growth.

How big is the opportunity?

Upstart Auto is working in a massive market: The loan origination opportunity in auto is worth $727 billion annually, so the company's $1.5 billion in loan volume guidance is peanuts compared to its potential.

This is a young company with a lot to prove, but with the better system that it has built on the back of artificial intelligence and machine learning, it looks poised to capitalize on an immense opportunity. If Upstart lives up to its potential over the next decade, investors could see Upstart Auto become one of the company's biggest revenue generators.

This article represents the opinion of the writer, who may disagree with the “official” recommendation position of a Motley Fool premium advisory service. We’re motley! Questioning an investing thesis – even one of our own – helps us all think critically about investing and make decisions that help us become smarter, happier, and richer.

"auto" - Google News

March 28, 2022 at 06:00PM

https://ift.tt/K035utF

How Important Could Upstart's Auto Business Be by 2032? - The Motley Fool

"auto" - Google News

https://ift.tt/ZfJwWQz

Shoes Man Tutorial

Pos News Update

Meme Update

Korean Entertainment News

Japan News Update

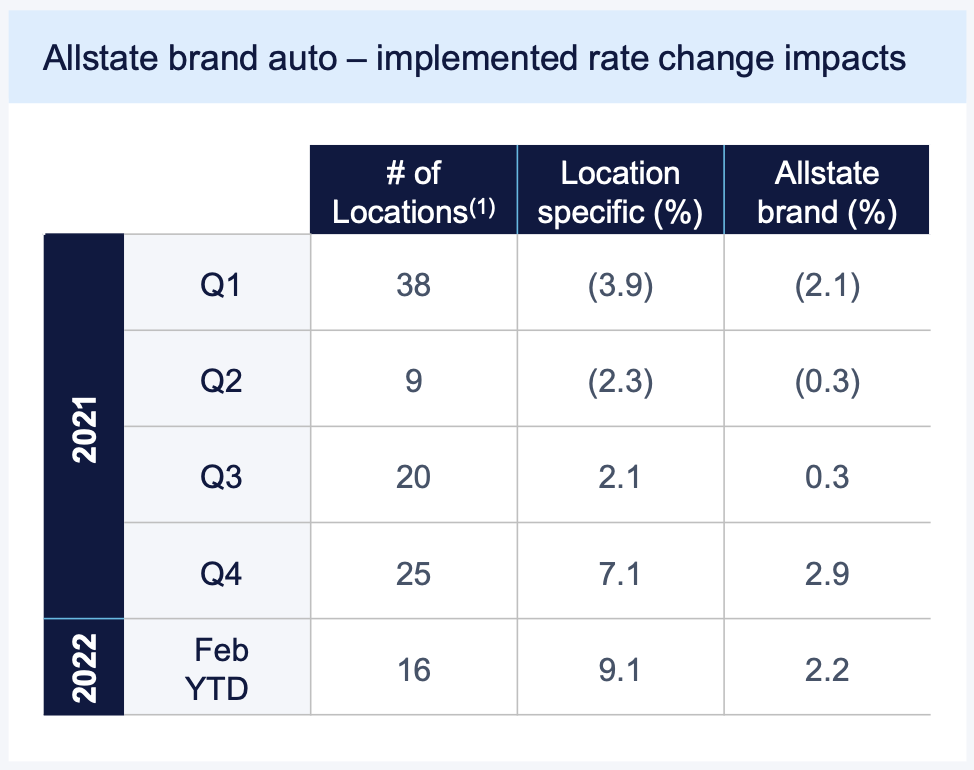

Allstate pursues auto insurance rate increases in bid to return to profitability - Repairer Driven News

Allstate continues to raise rates in response to increased loss ratios, company executives said during a special investor conference focused on auto insurance.

Since the fourth quarter of 2021, the carrier has received approval for 41 rate increases averaging 7.8 percent each across 34 locations, Allstate executives told investors during the March 17 call.

The increases of the past five months will bring in an additional $1.2 billion in premiums over the course of the year, according to Glen Shapiro, president of Allstate’s personal lines.

Mario Rizzo, executive vice president and chief financial officer, said Allstate has begun providing monthly reports on its auto insurance rates, and will continue doing so through 2022 “as we address rising loss costs.”

“We will disclose rates implemented each month, so you can have real time line of sight into our progress on increasing rates to improve auto margins,” Rizzo said.

Shapiro noted that, under the stay-at-home orders that accompanied the pandemic, Allstate saw “strong profitability in 2020 and early ’21.” That changed in the second half of 2021, “driven by inflationary pressure on severity.”

“To put that shift into perspective … we generated auto insurance underwriting income of $1.7 billion during the first half of ’21, and then an underwriting loss of $459 million in the second half of the year,” Shapiro said.

He noted that other large carriers had experienced the same shift, meaning that “we’re addressing margins at the same time as our competitors … the entire industry has started to take rate increases.”

Loss ratios, Shapiro said, rose eight points between the third quarter of 2019 and the third quarter of 2021. The increase in costs is being driven not by frequency, but by severity, he said.

Loss ratios, Shapiro said, rose eight points between the third quarter of 2019 and the third quarter of 2021. The increase in costs is being driven not by frequency, but by severity, he said.

Physical damage frequency remained below 2019 levels by 13.3% in the fourth quarter and 19.8% for the full year, he said. Although miles driven has rebounded from early in the pandemic, driving patterns have shifted, affecting claims.

“Non-rush-hour claims have essentially reverted to historical norms, and the increased portion of miles driven during times with less road congestion is likely one of the leading causes of a higher proportion of high-impact accidents and related injuries,” he said.

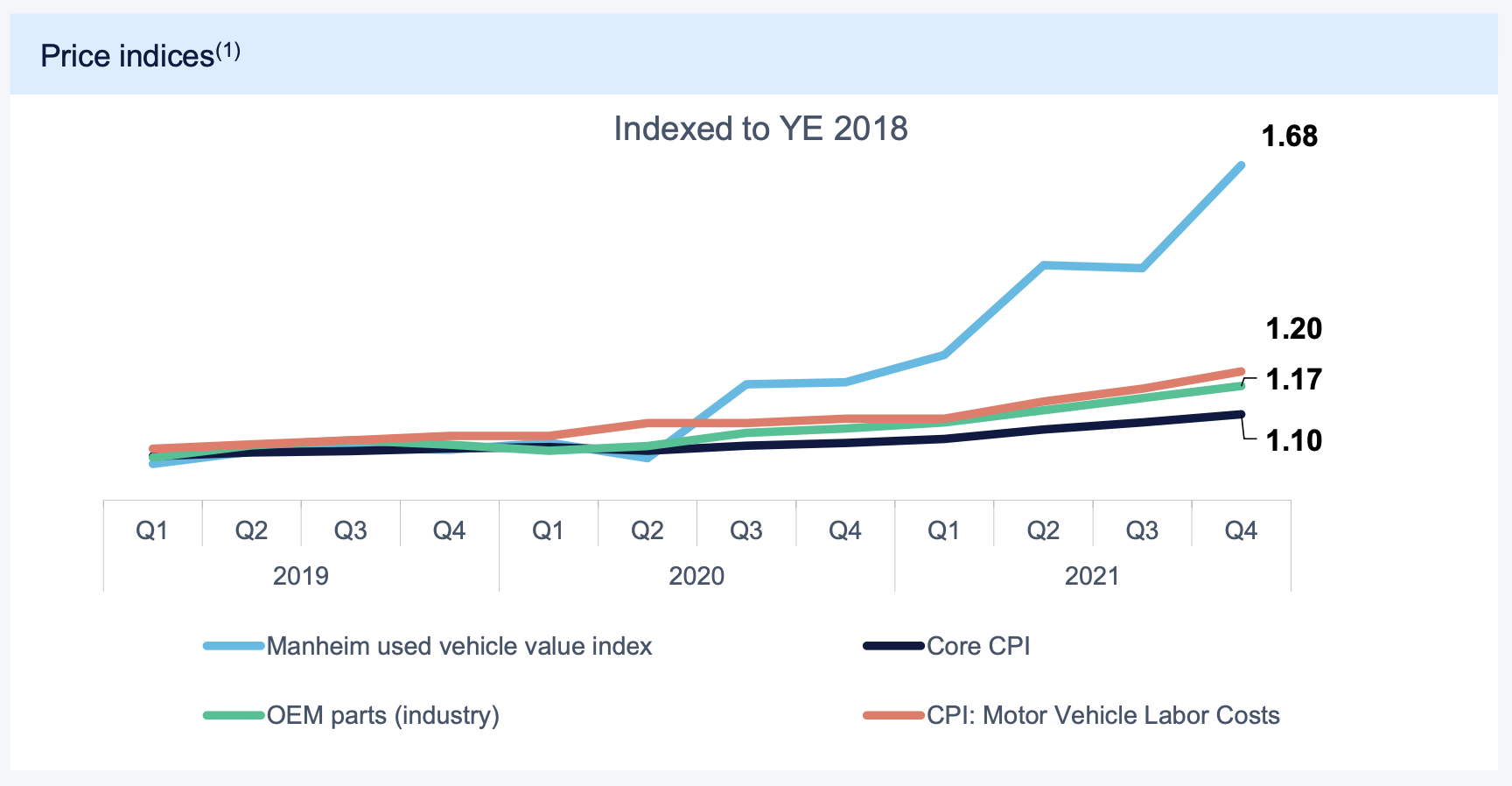

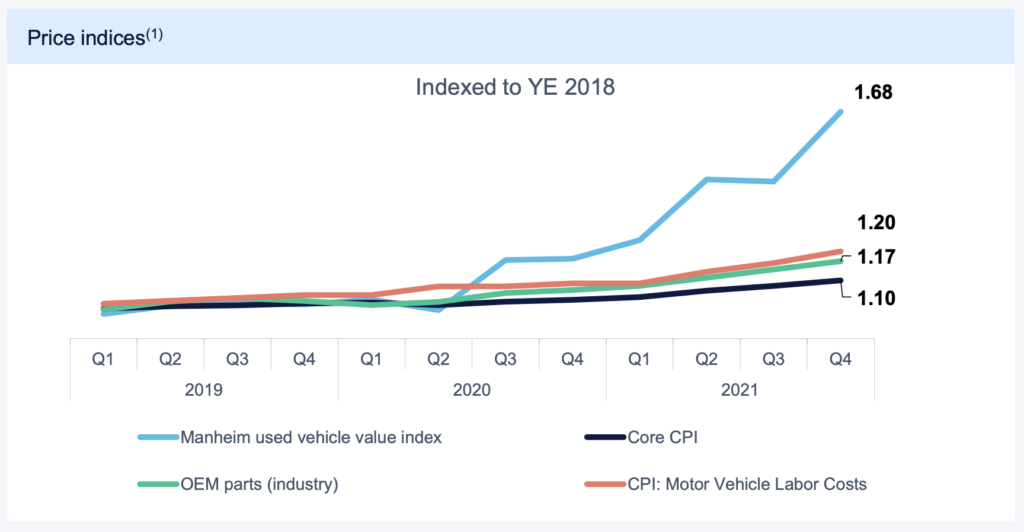

Eric Brandt, executive vice president and chief claims officer, said the increase in physical damage severity has added six points to the company’s loss ratio since 2019. One of the drivers, he said, is a 68% rise in the value of used cars since 2018.

“We’ve seen a dramatic rise in the value of used cars contributing to about 60% of the physical damage combined ratio increase on a pure severity basis,” Brandt said. “Higher speed accidents have resulted in more severe impacts, placing more cars in total loss category, which contributes to another about 20% of the increase in physical damage severity. This combination of higher used car values and harder hits has led to more total losses and a substantial increase in total loss of area. Lastly, supply chain shortages along with a competitive labor market have increased the price of car repairs, representing the remainder of the increase in physical damage severity.”

From a pandemic low of 86.0 in 2020, Allstate’s auto insurance combined ratio climbed to 104.3 in the fourth quarter of 2021, meaning meaning that the carrier spent $104.30 for every $100 it collected in premiums.

Julie Parsons, Allstate’s chief operating officer, noted that combined ratios were at 96 or higher in about half the states where Allstate writes policies in the second half of 2021. Between 2017 and the first half of 2021, nearly all states were at or below 96, she said.

In fact, in the third and fourth quarters of 2021, the states where the combined ratio was 100 or higher represent about 55% of Allstate’s written premiums, Parsons said. “We anticipate our comprehensive approach, including rates, will restore auto profitability to target levels,” she said.

Shapiro said Allstate plans to return to a combined ratio in the mid 90s, through raising rates, managing lost costs through claims effectiveness, and focusing on reducing expenses. “Increasing rates is definitely core to restoring margins, but we can moderate the impact for customers through claims excellence and reducing expenses,” he said.

Mitigating expenses, Brandt said, are the “predictive models” Allstate uses on the first notice of loss (FNOL) “to quickly and more accurately determine which vehicles are repairable and which ones should be totaled or sold for salvage.” He said the company’s data scientists had used proprietary data to improve total loss predictability at FNOL by more than 200% over the past year.

Echoing Shapiro’s remarks from Allstate’s fourth-quarter earnings call in February, Brandt told investors that the carriers is using “strategic partnerships with repair facilities and part suppliers which leverage Allstate’s scale.”

“We have a countrywide network in both parts and vehicle repair. We’re also in more than 30 markets with our own proprietary part supplier and of course we’re countrywide with our Good Hands repair network of body shops. For repairable vehicles, our estimating technology locates high-quality, cost-effective replacement crash parts,” he said.

Because parts costs account for half of repairs, any “incremental” savings have a “meaningful benefit” to Allstate’s margins, he said.

Brandt said Allstate expects to grow its data science team dedicated to claims by 125% over two years, beginning in 2020.

The company has seen “greater customer adoption” of its digital claim tools, such as photo-driven virtual estimating and “Virtual Assist,” a technology that lets body shops video chat with adjusters in real time. Those tools have led to a 1.2-point reduction in the claim expense ratio since 2018, Brandt said, generating a savings of $500 million.

More information

Images

Featured image provided by Kameleon007/iStock

Chart and graph provided by Allstate

Share This:

Related

"auto" - Google News

March 28, 2022 at 05:45PM

https://ift.tt/ZL4KWTm

Allstate pursues auto insurance rate increases in bid to return to profitability - Repairer Driven News

"auto" - Google News

https://ift.tt/ZfJwWQz

Shoes Man Tutorial

Pos News Update

Meme Update

Korean Entertainment News

Japan News Update

Sunday, March 27, 2022

How auto regulators played mind games with Elon Musk - The Washington Post

The regulators knew Musk could be impulsive and stubborn; they would need to show some spine to win his cooperation. So they waited. And in a subsequent call, “when tempers were a little bit cool,” the official said, Musk agreed to cooperate: “He was a changed person.”

Since that success in 2016, officials have learned to work with Musk, using a combination of pressure, flattery and threats to persuade him to comply with federal safety measures, according to a half-dozen former regulators, some of whom spoke on condition of anonymity to discuss sensitive matters. In the past six months, Tesla has issued at least a dozen voluntary recalls, a dramatic turnaround for a company known to quietly issue software updates direct to cars — without alerting the public — to fix sometimes alarming safety problems.

With about 2 million cars on the road, Tesla recently has experienced a wave of troubles: Cars using its driver-assistance features have slammed on the brakes for no reason and rolled through stop signs — the latter because Tesla programmed them to do so. A string of crashes into parked emergency vehicles is under investigation. And the cars’ batteries have been documented exploding in crashes and while parked in garages.

Such issues typically prompt NHTSA to investigate and sometimes to push for voluntary or mandatory recalls. If an automaker refuses to cooperate, NHTSA can impose cash fines of about $23,000 per day. The threat of fines — which can add up to nearly $115 million — generally works with traditional companies, the former officials said, but hasn’t proven effective when dealing with Tesla, an extraordinarily valuable company owned by the richest man in the world.

So NHTSA officials have turned to less conventional strategies to force the electric vehicle manufacturer to be more transparent about safety issues — a critical matter at a time when more than 50,000 drivers can now use Tesla’s “Full Self-Driving” software to navigate the nation’s public roads.

“Tesla is presumably smart enough to realize when they don’t have the upper hand anymore,” said Phil Koopman, an associate professor at Carnegie Mellon University whose focus includes federal auto regulations. “Tesla has a choice to make — they have to decide whether to cave or go to the mat. And the reality is, on [federal safety regulations] they’re going to lose.”

Tesla and Musk did not respond to specific questions in a detailed request for comment. Musk said in an email, “For the 100th time, please give my regards to your puppetmaster,” referring to Amazon founder Jeff Bezos, who owns The Washington Post. In a subsequent email, he also criticized The Post’s paywall for online articles.

NHTSA declined to make anyone available for an interview, citing ongoing investigations. But the agency issued written statements to The Post expressing its commitment to protect public safety.

Tesla has publicly touted the safety of its vehicles and its driver-assistance technology, boasting that it has won the highest possible score — five stars — in crash tests where NHTSA slams cars into barriers and then examines the results. Tesla also has said its cars have the lowest probability of injury of any car tested, though NHTSA has disputed that characterization.

Musk’s own attitude was part of the problem with efforts to enforce safety, the officials said. Some experienced personal encounters with Musk that escalated into yelling matches or otherwise proved unproductive because of the CEO’s skepticism about their findings.

NHTSA’s experiences with Tesla were unique among major automakers, the officials said. It was not rare for companies under scrutiny to fiercely push back against their findings, sometimes resulting in mandatory rather than voluntary recalls, they said. But with Tesla, issues as simple as a malfunctioning heat pump or noncompliant sound effects to alert pedestrians to a vehicles’ presence could result in stubbornness.

Tesla eventually issued recalls in both cases — decisions influenced by NHTSA, a spokeswoman said.

“NHTSA will ensure that vehicle manufacturers and developers prioritize safety while they usher in the latest technologies,” spokeswoman Lucia Sanchez said.

Regulators have been slow to take action on some software suites that power automated features, in part because they are wary of appearing to stifle emerging technologies, the former officials said. There also are few rules governing these technologies, further hindering efforts at regulation.

Since 2016, NHTSA has opened 31 special crash investigation cases involving advanced driver-assistance technology, according to data provided by the agency. Twenty-four have involved Tesla vehicles.

Safety experts and some of the former regulators who spoke with The Post raised concerns about “Full Self-Driving” in particular because of its experimental nature. Tesla says the software is in “beta,” meaning it is a pilot through which the company hopes to learn and improve its features for an eventual full release.

Lawmakers have pressed for more transparency regarding Tesla’s practices. In February, following a Post report on the cars’ sudden braking, Sens. Richard Blumenthal (D-Conn.) and Edward J. Markey (D-Mass.) criticized Tesla for putting software on the roads “without fully considering its risks and implications.” They urged NHTSA “to continue taking all appropriate action to protect all users of the road.” And they called on the Federal Trade Commission to launch an investigation into what they called “misleading advertising and marketing” of Autopilot and “Full Self-Driving” systems.

During much of the Obama administration, Tesla slid under the radar of federal safety regulators. As a niche automaker delivering at most tens of thousands of luxury cars per year, officials said it would not have ranked on the agency’s priority list, compared with high-volume automakers such as Ford and Toyota. From 2013 to 2015, there was just one recall per year for early Tesla Model S luxury sedans. Those recalls — which involved seat back mountings, charging equipment and incorrectly secured seat belts — compare with a total of 2,261 vehicle recalls over the same period, according to NHTSA data.

One early run-in set the tone for regulators’ interactions with Tesla. In 2013, Tesla claimed its Model S was the safest car ever tested by NHTSA.

Officials at the agency were dumbstruck, according to some of those who spoke with The Post. The agency issues up to 5-star ratings, but it does not take its designations beyond the star score.

At one point, two former officials recalled, NHTSA officials threatened to contact the FTC, which regulates marketing. “If Tesla wasn’t willing to pull the plug, FTC was probably going to take action,” one of the former officials said.

Tesla backed down.

But Tesla continued to make similar claims, including in 2019, when it said its Model 3 had the “lowest probability of injury of any vehicle ever tested” by NHTSA. The agency ultimately referred the automaker to the FTC. The FTC declined to comment.

NHTSA, meanwhile, focused increasing attention on the automaker as it built more and more cars, launching the Model X SUV in 2015 and steadily growing its production in the buildup to the mass market-aimed Model 3. The agency also had to deal with emerging issues, such as fires caused by road debris striking the cars’ underbodies, where the high-voltage battery is located. Musk wrote in a statement at the time that Tesla would introduce a fix to bring that risk “down to virtually zero.”

One official recalled that regulators were confused by Musk’s reluctance to address one battery-related issue. The only evident solution was to appeal to his sense of pride.

“NHTSA staff backs Musk into a corner and challenges his ego and says, ‘Wait, you can’t solve this?’ ” a former official said. “And the next day he has a solution.”

The Trump administration was even less hands-on. The NHTSA website lists only one recall for the 2017 through 2020 Tesla Model 3, then the automaker’s most popular model. Depending on the model year, there were up to eight recalls issued for the same car beginning May 25, 2021, after President Biden took office.

Under the Trump administration, career officials and top staff were reluctant to take a strong stance on a mounting catalogue of safety concerns, wary of appearing to target innovation and already under pressure from the president to ease regulations.

The officials said staffers were reluctant to take on a rapidly emerging automotive power with a massive public platform, worried they wouldn’t have the backing of top officials if they received a browbeating from Musk.

“My former staff felt they had nothing to do — twiddling their thumbs,” one former official said. “The professional staff — the career staff — wanted to do stuff either from a regulatory standpoint or investigation perspective” but were stymied.

Musk praised NHTSA as “great” in April 2021.

Then, things changed.

Although Labor Secretary Marty Walsh recently met with Musk and took a factory tour in Texas, Axios reported, Musk has criticized President Biden for leaving Tesla out of major events. Musk also has parroted Republican barbs, joking at one point Biden was “sleeping.”

Last summer, NHTSA began requiring companies such as Tesla to report on certain crashes involving automated features within one day of learning of the incident. Then in August, the agency launched an investigation into about a dozen crashes involving parked emergency vehicles while Autopilot was active. In a letter, it called out Tesla for pushing out a software update to help its cars better see emergency vehicles, without formally issuing a recall.

A surge of investigations, recalls and public admonitions has followed.

Former officials who spoke with The Post said Tesla’s haphazard approach has grated on some NHTSA staff, and the enforcement reflects an attempt at a course correction.

“The agency does hold a very firm line on [federal motor vehicle regulations], and I don’t think any of us want to live in a world where the automakers do essential recalls without going through that process,” said Bryan Thomas, who was communications director at NHTSA during the Obama administration. “If the car’s going to react differently at a stop sign tomorrow than it did today, you should know that as a driver.”

The former officials said NHTSA is not singling out Tesla. Instead, they said the agency is using a calculated approach to try to force the combative automaker to recognize findings that can’t be denied. That means picking targets — the seat belt chime, rolling stops, a windshield defroster — that may strike executives and even some owners as trivial. But those narrow targets offer an entree to larger issues that are not yet addressed by federal regulations, which often lag behind the latest software advances.

In February, NHTSA cracked down on a feature known as “Boombox,” which plays sounds that bystanders can hear — such as an ice cream truck jingle — but can drown out sounds that warn pedestrians of approaching vehicles. On Twitter, Musk decried the agency as the “fun police.”

Federal safety investigators from the National Transportation Safety Board have also focused their attention on Tesla. Late last year, NTSB Chair Jennifer Homendy wrote a letter to Musk calling out the company’s “inaction” on recommendations that would have added safeguards to the Autopilot system in response to the fatal 2016 crash with the tractor-trailer.

In a statement posted to its website at the time, Tesla called the death “A Tragic Loss.” The company defended the performance of Autopilot across the tens of millions of miles it had logged and emphasized that drivers should be prepared to take control of the vehicle at any time.

In September, Homendy expressed her concern about Musk’s approach to safety in an interview with The Post.

“I think Elon Musk is an incredible innovator," she said, expressing hope for "the ultimate success of [autonomous vehicle] technologies — which could save lives.”

But she also encouraged Musk to “really prioritize safety for his company," adding: "I don’t want to see lives lost in the meantime.”

"auto" - Google News

March 27, 2022 at 11:48PM

https://ift.tt/Eue8QKi

How auto regulators played mind games with Elon Musk - The Washington Post

"auto" - Google News

https://ift.tt/lgKenG5

Shoes Man Tutorial

Pos News Update

Meme Update

Korean Entertainment News

Japan News Update

Planners approve permits for auto repair buildings | News | avpress.com - Antelope Valley Press

LANCASTER – The Planning Commission approved Conditional Use Permit 20-11 for the construction of two 3,976 square-foot buildings for automotive repair on 0.53 acres of vacant land at the northeast corner of Division Street and Avenue J-5 in the commercial zone.

The Commission voted 5-0, with Commissioner Diana Cook absent.

The proposed project by applicant Julio Razo requires a conditional use permit because it would be within 300 feet of residentially zoned property, according to a presentation by Senior Planner Joceyln Swain at the March 21 Planning Commission meeting.

The surrounding land uses include the Lancaster Korean Church to the south; a locksmith to the north; single-family residences to the east; and an auto repair facility to the west.

The proposed buildings would be along the northern and southern property lines and set back approximately 10 feet from the property line along Division Street, according to a staff report. Each building would have approximately 3,536 square feet of shop area and 440 square feet of office area. Each building would contain four service bays. The project would include 2,461 square feet of landscaping throughout the site and the parking areas.

"auto" - Google News

March 27, 2022 at 06:00PM

https://ift.tt/2GgeEu6

Planners approve permits for auto repair buildings | News | avpress.com - Antelope Valley Press

"auto" - Google News

https://ift.tt/lgKenG5

Shoes Man Tutorial

Pos News Update

Meme Update

Korean Entertainment News

Japan News Update

Auto insurance refunds on the way | Localnews | heraldpalladium.com - Herald Palladium

[unable to retrieve full-text content]

Auto insurance refunds on the way | Localnews | heraldpalladium.com Herald Palladium"auto" - Google News

March 27, 2022 at 05:00PM

https://ift.tt/BPZJIuX

Auto insurance refunds on the way | Localnews | heraldpalladium.com - Herald Palladium

"auto" - Google News

https://ift.tt/lgKenG5

Shoes Man Tutorial

Pos News Update

Meme Update

Korean Entertainment News

Japan News Update

Auto body industry makes final push for fair reimbursement bill - GazetteNET

"auto" - Google News

March 27, 2022 at 09:30PM

https://ift.tt/RGBLUSv

Auto body industry makes final push for fair reimbursement bill - GazetteNET

"auto" - Google News

https://ift.tt/lgKenG5

Shoes Man Tutorial

Pos News Update

Meme Update

Korean Entertainment News

Japan News Update

Popular Posts

-

rest.indah.link Two girls operate the Giant Joystick at LABoral Art and Industrial Creation Centre, March 31, 2007 in Asturias, Spain. ...

-

rest.indah.link Microsoft's fascination with Windows and Android interop is not really new. Back during the Windows Phone era, Micros...

-

rest.indah.link DENVER — A surveillance camera mounted above the garage didn't deter a brazen car thief from stealing Erika Gebhardt...